Now THIS is a REAL housewarming gift. :)

Many seniors may not be aware of the various Alberta programs available to assist them with their optical and dental needs. I continually try to source “Hidden Gems” available yet not well advertised that are in place to assist our deserving seniors. This is just one of them.

To be eligible for the Dental and Optical Assistance for Seniors programs you must:

be 65 years of age or older

be an Alberta resident and have resided in Alberta for at least 3 months before applying

be a Canadian citizen or admitted to Canada for permanent residence (landed immigrant)

be approved to receive Seniors’ Financial Assistance programs

have an annual income within the limits allowed by the program

Read the Dental and Optical Assistance for Seniors brochure for more information.

Eligibility for the Dental and Optical Assistance for Seniors programs is determined by a senior’s ‘total income’ as reported to the Canada Revenue Agency (CRA) in the previous tax year.

‘Total income’ means the total income as defined in the Income Tax Act (Canada) and refers to line 15000 of an Albertan’s federal tax return.

For the 2023-24 benefit year (July 1, 2023, to June 30, 2024), your 2022 total income will be used to determine your eligibility. Table 1 outlines the total income guidelines for these programs and the benefits available.

Table 1. Marital status, income and benefits

|

|

Maximum coverage* |

Partial coverage* |

No coverage |

|

Single senior |

$0 to $31,080 |

$31,081 to $31,675 |

Over $31,675 |

|

Single couple |

$0 to $62,160 |

$62,161 to $63,350 |

Over $63,350 |

*More information on dental and optical coverage is available, see below.

To remain enrolled in the Dental and Optical Assistance for Seniors programs, you must have an active file with the Alberta Seniors Benefit program.

Use the Seniors Benefit Estimator to see if you are eligible for benefits.

To determine your eligibility for the Dental and Optical Assistance programs, you must first apply for Seniors Financial Assistance programs.

If you have already submitted the Seniors Financial Assistance application form, there is no need to apply again.

Eligible seniors are provided up to a maximum of $5,000 of coverage every 5 years for select dental services and procedures that maintain a reasonable level of dental health. When you are first enrolled in the program, the 5-year period will begin on the date of your first dental service funded under this program.

Every 5 years, your $5,000 of funding is renewed. If you do not use the full $5,000 in this period, the remaining amount will not carry over into the next 5-year period.

Dental coverage is based on the Dental Assistance for Seniors Program Fee Schedule, which establishes both the maximum fee amount and frequency of coverage for eligible services.

If you are eligible for maximum coverage, your funding will cover the maximum fee amount(s) for eligible procedure(s) found within the fee schedule. Maximum coverage may not cover the full fees charged by Alberta dental providers.

If you are eligible for partial coverage, your funding will cover 99% to 10% of the fee amount(s) for eligible procedure(s) within the fee schedule. Your percentage of partial coverage will depend on your 2022 total income.

Prior to receiving a dental service and/or procedure, it is important to ask your dental provider to submit a pre-authorization (cost estimate) to the Alberta Dental Service Corporation. This step will ensure the dental service and/or procedure is an eligible benefit covered by the program and will determine how much you will have to pay.

Basic dental services covered under this program include:

diagnostic services (examinations and x-rays)

preventive services (polishing and scaling)

restorative services (fillings, trauma, pain control)

extractions (simple and complicated)

root canals (endodontics)

procedures relating to gum disease (periodontics, root planing)

dentures (removable prosthodontics, basic full and partial dentures)

Dental services and procedures not found in the fee schedule and not covered under this program include:

dental crowns

fixed dental bridges

braces and orthodontics

dental implants

fluoride treatment

teeth bleaching and cosmetic procedures

inlays (gold or gems)

Dental providers may provide a dental service that is not an eligible benefit.

It is important to note the Dental Assistance for Seniors program does not provide full coverage of the fees charged by Alberta dental providers.

See the example below.

Table 2. A typical annual check-up with cleaning for a senior with maximum coverage under the Dental Assistance for Seniors program

|

Dental procedure |

2023 Alberta Dental Fee Guide rates* |

Maximum program fee schedule rates |

Senior’s portion |

|

Senior's portion total |

$59.04 |

||

|

Recall exam |

$73.85 |

$62.94 |

$10.91 |

|

Two bitewing radiographs |

$54.60 |

$43.00 |

$11.60 |

|

Two units scaling |

$154.42 |

$126.68 |

$27.74 |

|

One unit polishing |

$68.79 |

$60.00 |

$8.79 |

*These rates are found within the 2023 Alberta Dental Fee Guide. For more information on the Alberta Dental Association’s General Dentist Fee Guide rates, visit: Alberta Dental Association.

Based on the Dental Assistance for Seniors Program Fee Schedule, frequency limitations may apply for specific dental services.

Dental providers may choose to perform dental services more frequently than permitted under the program. The senior is responsible for the cost of these services if they choose to proceed.

All dental services and procedures supported by this program must be completed by a dental provider located within Alberta.

Eligible seniors are provided up to a maximum of $230 every 3 years towards the purchase of prescription eyeglasses. When you first enroll in the program, the 3-year period of coverage will begin on the date that you receive the first funded optical service under this program.

Every 3 years, your optical funding is renewed. If you do not use the full funding in this period, the remaining amount will not carry over into the next 3-year period.

If you are eligible for maximum coverage, you will receive up to a maximum of $230 of optical funding.

If you are eligible for partial coverage, you will receive up to a maximum of $115 of optical funding.

Optical funding covered under this program includes:

prescription eyeglasses

prescription sunglasses

prescription lenses (including contact lenses)

frames

eyeglass repairs

Optical services not covered include:

eye exams*

eye surgery

lenses for cataract surgery

accessories

magnifying devices

eye medication

non-prescription sunglasses

*Note: Seniors 65 years and older are eligible for one eye exam per benefit year (July 1 to June 30) through the Alberta Health Care Insurance Plan (AHCIP). For more information, review services covered under the AHCIP.

If you purchase prescription eyeglasses within the 3 years and you do not use your full funding at that time, you can use the remaining funds before the 3-year period ends.

Assistance with an additional set of eyeglasses within the same 3-year period may be provided to an eligible senior when they had cataract surgery that led to a change in prescription.

Read the Cataract surgery claims below for more information.

Alberta Health has contracted the Alberta Dental Service Corporation to be the benefit administrator for all dental claims and to provide you with information about the Dental Assistance for Seniors program and answer questions regarding dental claims and payment. Contact information is provided below.

Alberta Health has contracted Alberta Blue Cross to be the benefit administrator for optical claims and to provide you with information about the Optical Assistance for Seniors program and answer questions regarding optical claims and payment. Contact information is provided below.

When visiting a dental or optical provider, present your Alberta health card and inform the service provider that you are a senior enrolled in the Dental and Optical Assistance for Seniors programs.

The service provider can confirm your eligibility and level of coverage at the time of your appointment by submitting a pre-authorization to the benefits administrator.

Dental or optical offices may bill the benefit administrator directly for services provided to you. If your service provider accepts this method, you will only be required to pay any outstanding amount not covered by the program.

If your dental or optical provider submits a claim directly to the benefit administrators, skip Step 3.

Dental or optical offices may not bill the benefit administrator directly for services provided to you. If this occurs, you will be required to pay the full balance and submit your receipts for reimbursement. You or your service provider must also complete sections of a reimbursement form.

If your dental or optical provider does not submit claims directly to the benefit administrators, go to Step 3 below.

All dental and optical claims must be submitted within 12 months of an expense being incurred. If you do not submit the claim within 12 months, reimbursement will not be provided.

You may collect a reimbursement claim form from your dental provider or the Alberta Dental Service Corporation. Ensure the claim form is complete and includes your personal health number.

You can also submit the dental claim online directly to the Alberta Dental Service Corporation after creating an online account. The online account will track your remaining dental funding, if a previous claim has been paid, and allow you to update your address or banking information.

Get a reimbursement claim form from your optical provider or Alberta Blue Cross and submit it to the address included on the form (PDF, 176 KB). Ensure the claim form is complete and includes your personal health number.

You can also submit the optical claim online directly to Alberta Blue Cross after creating an online account through Alberta Blue Cross' Member site. The online account will track your remaining optical funding, if a previous claim has been paid, and allow you to update your address or banking information.

If you had cataract surgery after receiving funding within the same 3-year period and there is a change in your prescription, you may be eligible for additional funding. To be eligible for this additional funding, you must have a medical note confirming the date of your cataract surgery.

Your optical provider can submit this claim, along with the medical note, on your behalf directly to Alberta Blue Cross. This process is based on the optical provider entering the confirmed date of cataract surgery and uploading documentation confirming your cataract surgery.

If you were denied funding or were funded less than expected for a dental or optical claim, you can request a review.

To request an explanation of the income information used to determine your eligibility for the program, contact the Alberta Seniors Benefit program via:

Alberta Support Contact Centre

Hours: 7:30 am to 8 pm (open Monday to Friday, closed statutory holidays)

Toll-free: 1-877-644-9992

If you have questions regarding the outcome of a dental claim, the fee amount paid by the program or why a dental service was not approved, contact:

Alberta Dental Service Corporation

Phone: 1-800-232-1997

Email: claims@adsc.org

Fax: 780-426-7581

If your questions were not resolved after calling the Alberta Dental Services Corporation, you or your dental provider can request a review of your dental claim by writing to:

Alberta Dental Service Corporation

200, 17010 103 Avenue NW

Edmonton, Alberta T5S 1K7

Your dental provider may submit an exception review on your behalf if the Alberta Dental Services Corporation did not approve a dental service.

All requests are reviewed by the Alberta Dental Service Corporation Review Committee. The exception review request must include:

the dental treatment plan

clinical and medical rationale and diagnostic information that supports your exception review request

Note: Dental services not listed in the dental fee schedule that are provided to a senior before the request is reviewed by the Alberta Dental Services Corporation Review Committee will not be funded.

Each request is reviewed on an individual basis, taking into consideration the eligible dental options available, the medical necessity of the requested treatment, the overall oral condition of the mouth and all pre-existing medical conditions. The information submitted will be used to ensure the proposed dental exception is the most cost-effective service and sustainable for a prolonged period.

Your dental provider will receive a written response from the Alberta Dental Service Corporation Review Committee once a decision has been reached. If you have questions regarding the outcome of a dental exception, contact your dental provider or:

Alberta Dental Service Corporation

Phone: 1-800-232-1997

Email: claims@adsc.org

Fax: 780-426-7581

If you have questions regarding the outcome of an optical claim, the amount paid by the program or why an optical service was not approved, contact:

Alberta Blue Cross

Phone: 1-800-661-6995

If your questions are not resolved after calling Alberta Blue Cross, or you are requesting exception coverage for an optical service that was not approved or is not an eligible benefit, you can request a review of your optical claim by writing to the Optical Assistance for Seniors program:

Optical Assistance for Seniors

PO Box 3100 Stn Main

Edmonton, Alberta T5J 4W3

The program will review your written request and respond by letter.

Click the lower link to go to the live site.

https://www.alberta.ca/dental-optical-assistance-seniors#jumplinks-2

are two types of property sales that can occur when a homeowner defaults on their mortgage payments or fails to pay property taxes.

While both types of sales involve the forced sale of a property, there are some key differences between the two. Foreclosure is a legal process that a lender can initiate when a borrower defaults on their mortgage payments. In a foreclosure, the lender takes ownership of the property and sells it to recover the outstanding debt owed by the borrower. Foreclosures are typically initiated by banks or other financial institutions that hold a mortgage on the property.

On the other hand, a court-ordered sale is a legal process initiated by a court when a property owner fails to pay property taxes or other debts. In this case, the court orders the sale of the property to recover the outstanding debt owed by the owner. Court-ordered sales can also occur in divorce cases, where the court orders the sale of a jointly owned property to divide the assets between the parties. One key difference between foreclosures and court-ordered sales is that in a foreclosure, the lender is the one initiating the sale and is typically responsible for marketing and selling the property.

in a court-ordered sale, the sale is overseen by the court, and a court-appointed trustee is often responsible for marketing and selling the property. Another difference between the two types of sales is the timeline. Foreclosures can take several months to complete, while court-ordered sales typically move through the legal system more quickly. In terms of the potential risks and benefits for buyers, foreclosed properties are often sold "as-is" and may require significant repairs or renovations. Court-ordered sales, on the other hand, may offer a greater opportunity for buyers to inspect the property and negotiate the sale terms.

while both foreclosures and court-ordered sales involve the forced sale of a property, there are important differences to consider. It is important for buyers to conduct thorough research and seek professional guidance when considering these types of sales.

In my opinion, foreclosures and court-ordered sales may not be ideal options for first-time or inexperienced buyers. These types of sales often come with higher risks and can be frustrating to navigate, as banks and courts may not be motivated to facilitate the sale quickly. Even after completing due diligence and obligations with the property owners, buyers may encounter delays and a lack of respect from the seller's representatives.

Furthermore, in Calgary's current market, buyers may have to pay a premium for foreclosed or court-ordered properties due to the high demand and competition. In such cases, the "Fear of Loss" can influence bidding, driving up the price even further.

As a real estate professional, when clients approach me looking for "deals", I often recommend exploring distressed properties owned by private sellers instead. These properties may require some repairs or renovations, but with the right skills and effort, buyers can quickly build equity and create a valuable investment. If you feel you have the skills & qualifications to build up some "sweat equity" in your next home, contact us today and we will help you make that happen!

The federal government announced an annual 1% tax on real estate owned by any non-resident, non-Canadian, and considered vacant or underused. In some situations, this also applies to Canadian owners.

The Underused Housing Tax Act (UHT) requires individuals impacted by this tax to file an annual return, subject to certain exemptions, and pay a 1% tax on the property’s value. The filing deadline for the 2022 tax year is April 30, 2023.

Although the government suggested only non-residents would be affected by the UHT, the scope of the final legislation is broader. We recommend your clients speak with a tax professional if you or they believe it applies to them. Also, please keep in mind that some provinces/territories and municipalities impose similar vacancy taxes, and you should review these rules to better understand how they could impact your clients.

The UHT imposes a tax on every taxpayer who, on December 31 of a calendar year, is an owner of a residential property in Canada, unless the owner is an “excluded owner” or an individual who qualifies for one of several exemptions available under the Act.

Residential property owners can be categorized into two classifications — excluded owners and affected owners.

The Underused Housing Tax rules do not apply to “excluded owners”. These owners, including Canadian citizens and permanent residents, have no UHT reporting or tax obligation. A complete list of conditions classifying an excluded owner can be found on the Government of Canada’s UHT page.

All affected owners (mostly non-Canadian owners but includes some Canadian owners) are required to file a return for each residential property they own, even if they are not liable to pay any tax, due to qualifying for an exemption. A complete list of conditions classifying you as an affected owner can be found on the government’s UHT page.

This classification is further broken down into two groups:

Ownership of a residential property may be exempt from the Underused Housing Tax for a calendar year depending on:

Detailed information on each of these exemptions can be found on the government’s UHT page.

All affected owners must file a separate Underused Housing Tax return for each residential property they own in Canada for the calendar year. Not filing for the UHT by April 30, 2023 could result in a penalty of $5,000 – $10,000 per return, even if no tax is owing due to an exemption.

For more information, please review Canada Revenue Agency’s (CRA) new UHT page, which includes the new UHT return, technical guidance and other information.

Please note: on March 27, 2023 the government announced UHT penalties and interest for the 2022 calendar year will be waived for any late-filed returns and for any late-payments, provided the return is filed or the UHT is paid by October 31, 2023.

The article above is for information purposes and is not legal or financial advice or a substitute for legal counsel. The CREA Café team is responsible for the official blog of The Canadian Real Estate Association (CREA). The CREA Café is a cozy place for CREA to connect with our valued members and friends by sharing our thoughts and insights over a virtual cup of coffee.

March 27, 2023

Today, the "Honourable" Ahmed Hussen, Minister of Housing and Diversity and Inclusion, announced amendments to the Prohibition on the Purchase of Residential Property by Non-Canadians Act’s accompanying Regulations. The Act was passed by Parliament on June 23, 2022, and the Act and Regulations came into force on January 1, 2023, as part of the Government of Canada’s strategy to make housing more affordable for Canadians.

The accompanying regulations were developed for the Act to set out specific exceptions, definitions, and clarifications necessary to implement the prohibition. To enhance the flexibility of newcomers and businesses looking to add to Canada's housing supply, the Government of Canada is making amendments to the Regulations, to expand exceptions to allow Non-Canadians to purchase a residential property in certain circumstances.

These amendments will further support individuals and families seeking to build a life in Canada by pursuing home ownership in their communities sooner and addressing housing supply issues. These amendments came into force on March 27, 2023. The following amendments are being announced by the Minister of Housing and Diversity and Inclusion:

The amendments will allow those who hold a work permit or are authorized to work in Canada under the Immigration and Refugee Protection Regulations to purchase residential property. Work permit holders are eligible if they have 183 days or more of validity remaining on their work permit or work authorization at the time of purchase, and have not purchased more than one residential property. The current provisions on tax filings and previous work experience in Canada are being repealed.

We are repealing section 3(2) of the regulations, so the prohibition does not apply to all lands zoned for residential and mixed-use. Vacant land zoned for residential and mixed-use can now be purchased by non-Canadians and used for any purpose by the purchaser, including residential development.

This exception allows non-Canadians to purchase residential property for the purpose of development. The amendments also extend the exception currently applicable to publicly traded corporations under the Act, to publicly traded entities formed under the laws of Canada or a province and controlled by a non-Canadian.

For the purposes of the prohibition, with regards to privately held corporations or privately held entities formed under the laws of Canada or a province and controlled by a non-Canadian, the control threshold has increased from 3% to 10%. This aligns with the definition of ‘specified Canadian Corporation’ in the Underused Housing Tax Act.

“To provide greater flexibility to newcomers and businesses seeking to contribute to Canada, the Government of Canada is making important amendments to the Act’s Regulations. These amendments will allow newcomers to put down roots in Canada through home ownership and businesses to create jobs and build homes by adding to the housing supply in Canadian cities. These amendments strike the right balance in ensuring that housing is used to house those living in Canada, rather than a speculative investment by foreign investors.”

The Calgary real estate scene is constantly evolving. With the right approach and calculated decisions, it is possible to redefine the market and make it work for you. By understanding the market trends, taking calculated risks and staying informed, you can maximize your investment opportunities and make wise decisions when it comes to buying and selling real estate in Calgary.

Calgary's real estate market has been through plenty of changes recently. The downtown core has seen an influx of new condo development, while the suburban markets have been slower to recover from the economic downturn. Despite these challenges, there is still money to be made in Calgary real estate if you know where to look. For those looking to invest in the Calgary real estate market, it is important to understand the current trends and how they may impact your investment strategy. One trend that has been affecting the market lately is the decrease in oil prices. This has led to job losses and less money being spent on housing across Alberta. While this may seem like bad news for investors, it actually presents a unique opportunity for those who are willing to take on a little more risk. Now that we've identified some of the current trends affecting Calgary's real Estate scene, let's talk about how you can make them work for you! By understanding market conditions and making calculated decisions, you can achieve success as a real estate investor in Calgary. When considering any investment, always remember to do your research and consult experts before making any final decisions… after all, knowledge is power!

Calgary real estate is transforming, and the current market is the perfect time to take advantage of the opportunities available to savvy investors. With the right strategies and calculated decisions, you can take advantage of the changing market and create a lucrative investment portfolio. Whether you're a first-time investor or a seasoned veteran, you can find the perfect property to fit your budget and lifestyle. With the appropriate combination of research and proactive decision-making, you can secure an investment that will yield a strong return in the future. This is the perfect time to capitalize on the Calgary real estate market and redefine your future.

It’s no secret that the Calgary real estate scene is constantly changing. With fluctuating prices and rising competition, home buyers need to make calculated decisions when trying to make a successful purchase. To redefine the Calgary real estate scene, it’s important to consider all options when buying a home and to be smart about your decisions. That means doing your due diligence and researching the current market trends, looking at different neighbourhoods and understanding what’s important to you when it comes to making a purchase. With the right knowledge and understanding, you can make the best decision when it comes to buying a home in Calgary.

Calgary is a vibrant city where the real estate scene is no exception. When it comes to making calculated decisions in real estate, a little research and planning can go a long way. It is important to know the market and be aware of the current trends so that you can make the best decision possible. In Calgary, investors have the opportunity to capitalize on the city’s growing population, economic expansion and a wide range of housing options. By doing your research, you can make an educated decision about which property will provide the best return on investment. Whether you are looking for a rental property, a family home or a commercial property, you can find the perfect fit with a calculated decision. With the right research and an informed decision, you can redefine the Calgary real estate scene and reap the benefits of the booming market.

Making a calculated decision when it comes to real estate in Calgary is essential. Doing so requires a clear understanding of your needs and goals. Before you decide to take the plunge and make that investment, you need to ask yourself some important questions. What are you looking for in a home? What types of amenities do you need? Where is your budget? Once you have answered these questions, you can begin to narrow down your choices and make an informed decision that is right for you. With careful and calculated research, you can make a smart decision that will redefine the Calgary real estate scene, and you can be proud of your investment.

In today's ever-changing real estate market, it's crucial to stay ahead of the game by researching market trends and recent sales before making any big decisions. With the Calgary, real estate market, staying informed can have a profound impact on the success of your investment. By researching market trends and recent sales, you can make informed decisions that will help you maximize your return on investment. Furthermore, understanding how the Calgary real estate market works can help you determine when is the right time to buy or sell, allowing you to make the most of your real estate investments. By taking the time to research market trends and recent sales, you can make calculated decisions that will redefine the Calgary real estate scene and help you get the most out of your investments.

Finding a real estate professional who can help you make calculated decisions and redefine the Calgary real estate scene is an essential part of the process. A professional realtor will be able to provide you with the knowledge, expertise and resources you need to make informed decisions, allowing you to make intelligent investments that will increase your chances of success. A real estate professional can provide you with a comprehensive understanding of the Calgary market, as well as insights into the trends, prices and neighbourhoods. They can also help you negotiate the best possible deal and navigate the legal aspects of the transaction. With their help, you can make smarter decisions, redefine the Calgary real estate scene and achieve your real estate goals.

In today's Calgary real estate scene, technology has opened up a world of possibilities for the savvy buyer or seller. Thanks to the latest technologies, buyers and sellers can make informed decisions about their investments in the Calgary real estate market. By utilizing technology to research neighbourhoods, compare properties, and determine market trends, buyers and sellers can stay ahead of the competition and make calculated decisions that will benefit them eventually. Thanks to technology, buyers and sellers can redefine the Calgary real estate scene and make informed decisions that will help them to get the most out of their investments.

Negotiating the best deal possible in the Calgary real estate scene is all about making calculated decisions. This means that you need to be prepared with the right information and take the necessary steps to ensure you are getting the best value for your money. Knowing the market, researching comparable properties, and understanding the local laws and regulations are key to making sure you get the best deal. Professional real estate agents can provide invaluable insight, advice and negotiation support to ensure that you get the best deal on your purchase. By taking the time to do your research, you can redefine the Calgary real estate scene with informed decisions, and get a great deal when buying a new home.

Making a calculated decision to purchase a property in the Calgary real estate market is a great way to redefine your lifestyle. With the right strategies in place, you can find the perfect property and get the best value for your money. With the appropriate know-how, you can make an informed decision and be confident in your purchase. Starting with a good plan, you can close on your new property with ease. You can rely on the expertise of a real estate professional to help you make the right decisions and to ensure that your purchase is successful. Don’t let the Calgary real estate market overwhelm you; make a calculated decision and redefine your life in no time!

The Calgary real estate market is a dynamic one, and if you are considering buying a home, you can benefit from making calculated decisions. By redefining the real estate scene in Calgary with your decisions, you can make the most of your investment. With careful consideration, you can make the best use of your money and find the right property for you and your family. Investing in real estate can be a rewarding experience, and with the right strategy, you can make the right decisions to make the most of your investment. Take the time to research the market and consider all the factors that will impact your decision. With the correct approach, you can redefine the real estate scene in Calgary and make the most of your investment.

The decisions Canadians make on their mortgage in 2023 are in large part dependent on the mortgage rate forecast. It’s a decision that will affect homeowners for several years to come and could lead to thousands of dollars in mortgage interest savings.

Here we will look at where mortgage rates are likely headed, based on a current January 1, 2023 review of economics, years of in-depth mortgage market study, and working with thousands of mortgage files.

Historical context: Mortgage rates are forecasted to increase further in 2023, but rates are likely to gravitate lower over the long term to a historical trend in the low-mid 3% range.

The market consensus on the mortgage rate forecast in Canada (as of January 1, 2023), is for the Central Bank to increase mortgage interest rates by another 0.25%, to a 4.50% high in early 2023, and may go higher if inflation is not on track to drop less than 4.50%.

Early signs of economic slowdown and lower mortgage rates.

How to reduce your risk against mortgage interest rate increases, best position yourself in this rate cycle, and save the most on your mortgage.

To help determine mortgage rate forecast, one of the best perspectives we have available is a historical one.

During the great recession of 2008, the financial system and economy as a whole required bailouts and stimulus as never before seen, just to keep running. Thankfully, the stimulus did its job, and the economy rebounded and got back on track. However, between 2008 and 2019, for over 10 years, there was very low or stagnant GDP growth, and interest rates remained low accordingly.

Now in an era of COVID, in 2020 – 2023 we witnessed a similar massive economic bailout. The difference this time is the stimulus was far greater, with over 40% of dollars ever created between 2020 – 2022.

However, in part due to a literal shutdown of the economy and of supply chains at one point, and difficulty rebooting these supply chains, along with the unfortunate war in Ukraine and supply issues in the housing market, there is much more inflation as the economy stabilizes.

This inflationary difference will be discussed in more detail just below. However, the main point here is that historically, when there is a massive new government and private debt layered upon already massive debt, this can perpetuate dependence on yet ever cheaper debt to stimulate the economy. It can lead to long-term economic stagnation and, importantly, to a ‘magnifying effect’ of increased rates.

More specifically, with 5 times more debt in the economy today, adjusted to inflation, than in the 1980s and early 90s, a single 0.25% rate increase makes a 5 times bigger impact than it did when debt levels were a fraction of current levels. Accordingly, there is significant long-term pressure for rates to remain low.

From another historical perspective, when rates increased in the 1980s from a base point of 10% to a 20% high point, this represented a 2x rate increase. However, a rate increase in 2022 – 2023 from a base point of 0.25% to 4.50% represents a 16x rate increase, which will have a much greater shock to the economy.

*If you'd like to be put in contact with one of our preferred mortgage broker specialists, please reach out to me.*

We will likely see this prime rate increase when the Central Bank meets on January 25, 2023. There is some early speculation that there could be an additional 0.25% increase on March 8, 2023, however, it is too early to forecast this second 2023 rate increase.

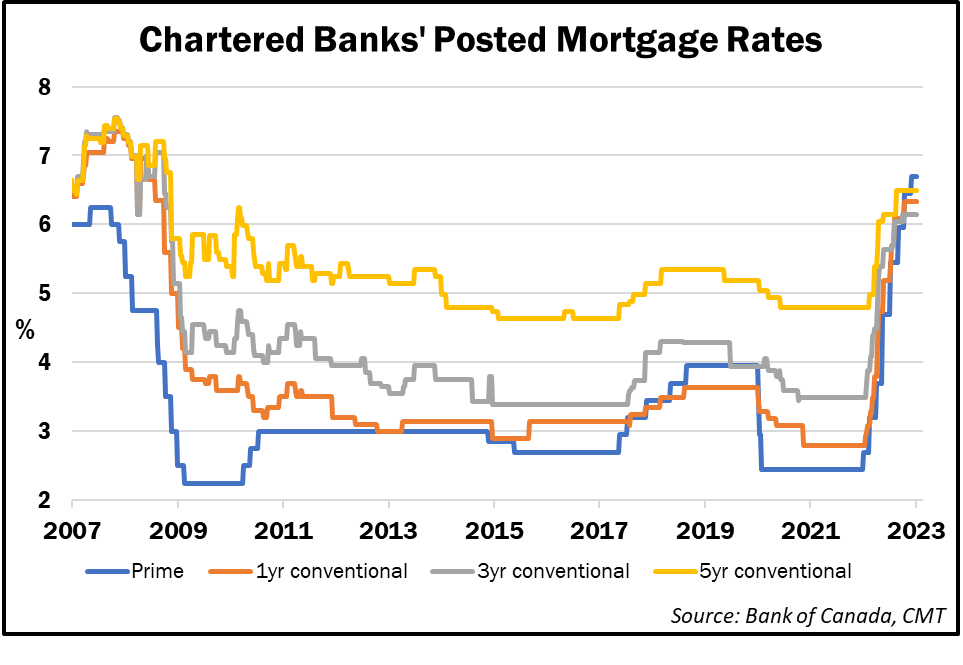

The main tool we have when reading the current mortgage rate market is the Government of Canada Bond Yield. The Canadian bond is a government debt security that pays a return to an investor. The ‘%’ based return is called the ‘yield’ and it is considered to be one of the safest investments because the Government would have to go bankrupt, in order for it not to pay its investors.

The Government of Canada's 5-year Bond Yield factors in all known economic data on a day-to-day, and even a minute-to-minute basis. Simply put – when the market/ bond traders think that the Central Bank of Canada will increase rates, the Bond Yield increases. When the Bond market thinks the Central Bank rate will decrease, then the yield drops. In other words, the Bond yield trades, or is priced in anticipation of where the Central Bank of Canada rates will move. The Central Bank of Canada makes its rate decisions, based on the status of the economy.

Currently, as seen in the Yield chart below, the Canadian Bonds are priced in anticipation of a further 0.25% increase in Central Bank of Canada rates in early 2023 or perhaps slightly higher.

With lower spending comes a slowing economy and lower inflation, and eventually, lower mortgage interest rates.

Current high rates will lead to lower rates – by design.

As of January 2023, there is a growing consensus among big banks that a recession in Canada will happen in 2023. The big banks have a unique real-time view of massive amounts of cardholder spending data and are well-positioned to report on economic trends sooner. In summary, what we are hearing is that spending is decreasing significantly due to higher costs throughout the economy and higher interest rate expenses, to the point of an overall economic slowdown.

As consumer demand drops, prices of many economic inputs such as oil, copper, steel, silver, lumber, microchips, shipping costs and many other commodities have fallen drastically. These trends are very anti-inflationary. However, housing costs (ie. rents), food costs and travel/leisure activity continue to be strongly inflationary. Likely there will be a point in 2023 when these more inflationary areas of the economy cool off.

It is known in economics and recently mentioned by the Central Bank of Canada, that it takes approximately 1 year for a single interest rate hike to ‘trickle through’ or have a full effect on slowing an economy. While the first small 0.25% interest rate hike in Canada happened in March 2022, as of January 2023, we have really only seen about 9 months of effects of the more significant ‘super-sized’ rate hikes, let alone the effects of a full year of multiple rate increases. So it is important to keep in perspective that:

(1) The previous rate hikes we have seen have not had their full effect on slowing the economy, and we are already seeing a recession on the near-term horizon.

(2) The markets are expecting another 0.25% of a rate increase before stopping.

Accordingly, the narrative is also shifting away from the likelihood of a ‘soft recession’ in 2023 towards a harder-felt recession. At the point of a more severe recession, inflation is likely to be reduced significantly.

What goes up to slow the economy, will eventually come down to stimulate the economy.

The Central Bank of Canada (and the Federal Reserve in the USA) is determined to fight inflation, which is why they are seen as slamming the breaks on the economy as a whole. There is no doubt this, unfortunately, will be painful for many. However, low inflation is needed on a foundational level to enjoy another long-term run of low interest rates.

Eventually, the Central Banks will begin lowering rates again to stimulate the economy and pull us out of the recession. This means lower mortgage interest rates.

More specifically, once the Central Bank reaches its peak rate or ‘terminal rate’, historically, it takes on average 6 months for the Central Bank to start lowering rates again.

In 2023, Bond markets are currently projecting the first Central Bank rate drop in November. This would mean a full 10 months at the peak rate – longer than the 6-month peak rate average.

However, to take a more careful and conservative projection, it could be January 2024 before the first Bank of Canada rate drop.

So given current market conditions, a good reference point would be between November 2023 and January 2024 for the first-rate drop.

However, if the economy slows harder and faster than expected, we could see the Central Bank lower rates sooner in 2023.

While the variable rate mortgage is directly affected by the Central Bank decisions, we will likely see 3-5-year fixed rates generally float lower throughout 2023. Because fixed rates are ‘pegged’ to the Government of Canada Bond Yields and Bond Yields trade in anticipation of Central Bank rate decisions, we will see fixed rates move lower much sooner.

Rates will not normalize at the lowest levels seen during COVID-19. However, as fixed mortgage rates approach a highly restrictive 5.5 – 6% range, the expectation is that rate normalization may occur into the low to mid ‘neutral rate’ range, or in the low 3% range for mortgage rates.

The CIBC Capital Markets projection from April 2022, seen just below, illustrates a good representation of this forecasted rate trend. However given stubborn inflation, the Central Bank rate peak will clearly be higher than in the numbers indicated in the chart:

Again, while the exact numbers are not coming in as was expected in April 2022, the main thing to note from the chart is that the rates and bond yields are increasing into 2023, but then towards the end of 2023 and into 2024, the bond yields are forecasted to drop, prompting a decrease in the Central Bank of Canada rate. This bigger-picture rate trend is the primary idea behind the chart.

At this time of higher rates, unfortunately, there is no good low rate to lock into. With this said, a calculated approach may be considered to position yourself to take advantage of lower rates once they begin to fall.

According to the Central Bank, it could take until late 2023 and into 2024 for inflation to fall substantially and for their prime rates to drop.

The traditional thinking is that a 5-year rate is a safer bet. However, from the ‘rate drop’ perspective analyzed, if you lock in a higher rate for too long, there is a risk of paying too much.

Therefore a shorter term, 3-year fixed rate, for example, could position you better to renew into a lower fixed rate in 3 years’ time. For example, if your rate today is locked in at 4.59%, you would not see further upside on your rate for the next 3 years. This zero upside potential comes with the peace of mind many Canadians are looking for with their rate.

With this said, it is likely that rates will be down, perhaps 1% or even more in 3 years time, in 2026. So on your renewal date, at the end of the 3-year term, you would be better positioned to renew at a lower rate and potentially save thousands of dollars, versus remaining locked into a higher 5-year fixed term, for another 2 years.

For those with a higher tolerance for risk, a variable rate is worth considering because the savings could be substantial.

As we near the end of the most stunning rate increase cycles in history, the variable rate should stabilize. Then, as soon as the rate begins to fall, perhaps in late 2023 or early 2024, the variable rate holder will benefit immediately. This ‘lower rate sooner’ potential could lead to more savings than locking in even a shorter-term fixed rate.

Given over 40 years of historical rate data, as seen in a York University study on Canadian interest rates, the variable rate is likely to lead to more significant savings over the medium–long term.

There is certainly the potential for substantially more savings in the variable, but with higher variable rates currently and another 0.25% increase projected in January, it will take a thicker skin in 2023 to realize these savings over the next 1-3 years

prevents non-Canadians from buying residential property in Canada for 2 years starting on January 1, 2023.

The Government of Canada has passed a new law to help make homes more affordable for people living in Canada. The Prohibition on the Purchase of Residential Property by Non-Canadians Act prevents non-Canadians and corporations controlled by non-Canadians from purchasing residential property in Canada for 2 years, Ensuring the housing market remains available to Canadians

In developing the accompanying regulations, the Government reached out to Canadians for their feedback. A detailed consultation document containing specific policy proposals intended for the regulations was available for comment for 4 weeks in August and September 2022. The consultation process received approximately 200 written submissions from individuals and stakeholders.

The Regulations will also come into force on January 1, 2023. The Act and its regulations will be repealed after 2 years.

For more details, read the Regulations in the Canada Gazette.

The Prohibition on the Purchase of Residential Property by Non-Canadians Act prevents non-Canadians from buying residential property in Canada for 2 years starting on January 1, 2023.

The Act defines residential property as buildings with 3 homes or fewer, as well as parts of buildings like semi-detached houses or condominium units. The law does not prohibit the purchase of larger buildings with multiple units.

The Act has a $10,000 fine for any non-Canadian or anyone who knowingly assists a non-Canadian and is convicted of violating the Act. If a court finds that a non-Canadian has done this, they may order the sale of the house.

Please note: This does not apply to non-Canadians who are looking to rent.

The information contained on this site is for general guidance only and is not to be construed as legal or other professional advice. It should not be used as a substitute for consultation with legal or other competent advisers. Before making any decision or taking any action, you should consult a professional.

CMHC is not responsible for any errors or omissions in connection with the use of this information. All information on this site is provided "as is," with no guarantee of completeness or accuracy.

CMHC won’t be liable to you or anyone else for any decision made or action taken in reliance on the information on this Site.

Many buyers are not aware that they will be denied insurance coverage on their purchase if one or more of these items are found in the home. Therefore, your mortgage company will not fund your mortgage until these deficiencies are rectified. One of the major issues is electrical.

If your Calgary home purchase has one or more of the following, you will not be insurable. 60 AMP service panels have to be upgraded to a minimum of 100 AMP panels. Many of the newer Calgary homes are installing 200 AMP service panels due to today's demand for all the new electronics in the homes. Be aware as well, that when you upgrade the panel, you also have to upgrade the feed from the street to your home and the drop into your meter. This can be several thousands of dollars cost.

If your new Calgary home purchase has aluminum wiring in it, you will also be denied bound coverage. Aluminum wiring was installed starting in the 1960s but was outlawed in Canada in the late 1970s because it contracts and expands more than copper wiring, which leads to loose connections, arcing, and ultimately fire.

Copper wiring has been used since the banning of aluminum. Some copper may "appear" to be aluminum but is only coated in nickel for specific applications. It increases copper's resistance to corrosion and enhances its strength. Calgary homes after the late 1970s have copper wiring but some still "may" have 60 AMP service panels, which will have to be upgraded to a minimum of 100 AMP.

Here we are taking a step back in time. Calgary home insurance companies do not like this era. Knob & tube wiring was predominant from the early 1900s up to the late 1950s. This is a very dangerous type of wiring to have in a home as it has no grounding and all connections are in the open. This makes your home very prone to catching fire when the wiring shorts out. Unlike today's copper wire connections that must be in an accessible, sealed junction box.

Poly B is the water line that you most likely have in your Calgary home if it was built between the mid-1970s to 1998. If your home was built prior to 1975 it will not have Poly B. However, we have found some homes relocated onto new foundations that have been extensively upgraded and classified as "newer" homes still have some Poly B. This pipe is prone to a short life and may decay at connections and or just spring a leak. The government of Canada officially banned Poly B™™ in 2005.

Upon the banning of Poly B in Calgary homes, insurance companies are looking for either older copper lines and/or the Pex lines that replaced Poly B. Pex is a plastic type of line that is easily installed with either crimp rings or shark bite fittings. It is estimated that approximately 148,000 homes in Alberta had Poly B installed in them. Ultimately, one way of usually detecting if the home has Poly B is to go to the utility room and look towards the ceiling. If you see light to mid-grey plastic piping, it probably is Poly B. It will most likely be stamped on it as well. Another area to inspect is under the sinks to see what is connected to the faucets.

In summary, I would caution all buyers to enlist the services of a "qualified" home inspector as part of your conditions on the Offer to Purchase. Upon request, I usually refer to Cliff Keveryga as one of Calgary's most qualified inspectors. I feel very confident that my 40 (+) years in and around the trades are a great comfort and asset to my clients when we are previewing properties. My background has consistently saved unnecessary headaches and frustration for my buyers as we are able to quickly eliminate these homes as an option.

In these tough times, people are looking at new & different approaches to get through them. This is one temporary fix that may work for some. As the number of properties listed through short-term rental services like Airbnb and VRBO continues to grow, it’s natural for homeowners to wonder if they, too, can extract additional value from their homes. Have an extra bedroom, guesthouse or vacation property that sits vacant most of the time? Want to rent out your condo a few weekends a year to make a bit of extra cash? No matter your specific circumstances, here are some important dos and don’ts.

This includes answering questions for potential guests, perfecting your listing, outfitting your property for guests, helping your guests check in and out, and troubleshooting for them during their stay.

Whether you’re living in a downtown condo building or a quiet, suburban area, your neighbours can kill your listing if you’re not careful. Be considerate when it comes to points of contention like noise and parking, set clear house rules for your listing, and be selective about the types of guests you target and to whom you ultimately rent.

Make sure your listing appeals to the type of guests most likely to book with you, and least likely to cause headaches for you and your neighbours – business travellers in downtown areas, for example.

Make sure you have the essentials – including things like smoke alarms and CO detectors, a working TV with streaming capabilities, reliable Wi-Fi, and coffee – as well as amenities that will set your listing apart from the competition.

These should not be overly restrictive, but make sure you indicate what is not allowed. Things to address include smoking, off-limit areas, quiet hours, extra guests and pets.

Run out of toilet paper, napkins or paper towel

This is one of the easiest ways to ruin a guest’s experience and ensure a negative review for your listing.

Airbnb offers free host protection insurance of up to USD 1 million, but certain things – such as property damage from pollution or mould, and intentional damage or injury – are not covered under the policy. Talk to your home insurance company about options for additional coverage.

People lose things, including keys, so make sure you’re ready with a backup plan. Lockboxes that guests can access that contain a spare key will go a long way towards improving your guests’ experience and making your life easier.

People appreciate their privacy, so barging in on a guest is sure to sour their experience. Try to avoid visiting your listing during a booking unless there is an emergency.

Forget to provide towels

Just like any hotel room, clean bath towels and washcloths are a must to keep your guests happy.

This requires regular monitoring and updating, as market conditions are constantly changing. Too high could mean extra vacant days, but too low could mean you’re not maximizing your earning potential. Third-party pricing companies, such as Wheelhouse, are also available for a small fee for hosts who want to eliminate most of the guesswork.

Definitely, before committing to a lawyer as with any professional, you want to know how much they will charge for their services and do they have the required experience/knowledge. Only then you can make the crucial decision about whether or not this real estate lawyer is a good match for you. Here are a few tips for you about the disposition of real estate attorneys and their rates.

Real estate purchases

Real estate sales

Land transfers

Refinances

Mortgages

Before you enter into an agreement with your real estate lawyer, make sure you know what their fees include. The full complex of services involves the following, and occasionally more: 1st – all regular disbursements; 2nd – file administration costs; 3rd – document fees; 4th – photocopies; 5th – fax; 6th – courier charges; 7th – land title fees to register title and mortgage; 8th – approximately 2 hours of consultation to help you resolve various issues related to your sale or purchase; You should also keep in mind that there may be some additional fees for out of town services.

It is always better to discuss such issues with your real estate lawyer beforehand. This way you will avoid uncomfortable situations, and unexpected costs and will know in advance exactly what you are paying for. Occasionally, specialized services may not be included in the standard price so it is always a good idea to double-check everything.

It is perfectly understandable that everyone wants to save money at any cost. People, contrary to all logical rules, start searching for excellent quality services with great discounts. Sometimes they get lucky, but usually, it doesn’t work that way. For small fees, you usually get the equivalent service. There are many cases where clients were over-charged for the initial quote. This is because the real estate lawyers were not qualified in the real estate field. Some purported real-estate lawyers have even prepared fraudulent documents, and at the end of the day, the client ended up with significant ramifications.

To be on the safe side and avoid such misfortunes, do not get fooled by cheap service fees. Check everything carefully and only then, make your choice. Many times the cheap way out ends up costing you double and more.

Real estate transactions can be quite stressful. For that reason, your real estate solicitor should be a seasoned real estate professional and be qualified to represent your best interests. When handling your residential or commercial transaction, he/she should;

Take control of and draft all documentation

Represent your best interests and always have your back

Consult and advise you on potential risks & obligations

Help and advise you on how to avoid any such risks

Closely collaborate with other professionals involved in the process of a real estate deal.

Throughout the entire process of your sale/purchase, you are going to encounter various professionals. The most relevant provision here is to make sure they are the people who understand and hear your preferences and demands. Only then will you have an agreeable encounter.

At first glance, domestic purchase contracts are merely a formality necessary to buy or sell real estate property. However, it is not as easy as it may appear. So, the residential purchase contract is one of the key documents that protect you and your rights when it comes to any legal dispute. Secondly, it sets the rules that govern how the dispute is resolved. So, even if you don’t hire a real estate agent to help you with selling/buying a house, you should consult a real estate lawyer and ask him to draft the contracts for you. Those who do decide to hire a professional real estate agent – don’t worry. Your Realtor will use the appropriate AREA (Alberta Real Estate Association) contracts which comply with all the legislation and protect “everyone.”

When it comes to the litigation process, ensure that a professional real estate lawyer in this field represents your interests. It is recommended to work with a litigator who has already had similar cases to yours. It will give you more confidence that together, you will win your case. Litigation in real estate disputes requires the full and immediate attention of your lawyer. The sooner he begins dealing with the matter, the better the results will be. A suitable research process can gain valuable information for you.

The litigation process can be started for various reasons. The most frequent are commission and deposit disputes. Also, there are many cases of “Breach of Contract”, improper measurements, etc. You are strongly advised to engage a professional lawyer to represent you as there also may be real estate disputes caused by hidden or builder defects. Such points should be examined and prevented beforehand, and a professional team consisting of your realtor, home inspector, and lawyer will help you. There are many other issues that real estate agents and lawyers can enlighten you on.

In fact, the real estate area of interest is a separate science and many educated people are being trained for years to become true professionals. Such real estate agents work for Calgary’s CIR Realty, like Ron Christensen. So, if you have any questions or are ready to proceed – contact, Ron and he will take the reigns for you, “From Sign Up to Sign Down”!