What is happening in the world of borrowing monies for your mortgage in Canada with the skyrocketing interest rates?

The decisions Canadians make on their mortgage in 2023 are in large part dependent on the mortgage rate forecast. It’s a decision that will affect homeowners for several years to come and could lead to thousands of dollars in mortgage interest savings.

Here we will look at where mortgage rates are likely headed, based on a current January 1, 2023 review of economics, years of in-depth mortgage market study, and working with thousands of mortgage files.

These 4 main predictions will be reviewed (fully updated for Winter – Spring 2023):

Historical context: Mortgage rates are forecasted to increase further in 2023, but rates are likely to gravitate lower over the long term to a historical trend in the low-mid 3% range.

The market consensus on the mortgage rate forecast in Canada (as of January 1, 2023), is for the Central Bank to increase mortgage interest rates by another 0.25%, to a 4.50% high in early 2023, and may go higher if inflation is not on track to drop less than 4.50%.

Early signs of economic slowdown and lower mortgage rates.

How to reduce your risk against mortgage interest rate increases, best position yourself in this rate cycle, and save the most on your mortgage.

Historical context: Mortgage rates in Canada are forecasted to gravitate towards historical lows for the long term of 5 – 10 years.

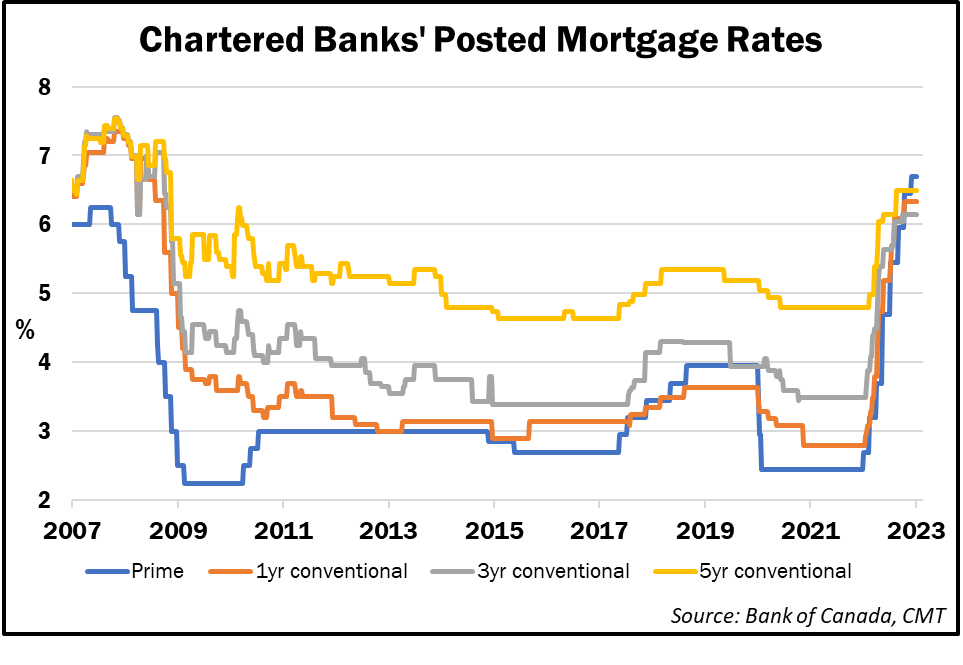

To help determine mortgage rate forecast, one of the best perspectives we have available is a historical one.

During the great recession of 2008, the financial system and economy as a whole required bailouts and stimulus as never before seen, just to keep running. Thankfully, the stimulus did its job, and the economy rebounded and got back on track. However, between 2008 and 2019, for over 10 years, there was very low or stagnant GDP growth, and interest rates remained low accordingly.

Now in an era of COVID, in 2020 – 2023 we witnessed a similar massive economic bailout. The difference this time is the stimulus was far greater, with over 40% of dollars ever created between 2020 – 2022.

However, in part due to a literal shutdown of the economy and of supply chains at one point, and difficulty rebooting these supply chains, along with the unfortunate war in Ukraine and supply issues in the housing market, there is much more inflation as the economy stabilizes.

This inflationary difference will be discussed in more detail just below. However, the main point here is that historically, when there is a massive new government and private debt layered upon already massive debt, this can perpetuate dependence on yet ever cheaper debt to stimulate the economy. It can lead to long-term economic stagnation and, importantly, to a ‘magnifying effect’ of increased rates.

More specifically, with 5 times more debt in the economy today, adjusted to inflation, than in the 1980s and early 90s, a single 0.25% rate increase makes a 5 times bigger impact than it did when debt levels were a fraction of current levels. Accordingly, there is significant long-term pressure for rates to remain low.

From another historical perspective, when rates increased in the 1980s from a base point of 10% to a 20% high point, this represented a 2x rate increase. However, a rate increase in 2022 – 2023 from a base point of 0.25% to 4.50% represents a 16x rate increase, which will have a much greater shock to the economy.

*If you'd like to be put in contact with one of our preferred mortgage broker specialists, please reach out to me.*

As of January 2023, the market consensus on the mortgage rate forecast in Canada is for the Central Bank to increase mortgage interest rates by another 0.25% in 2023 from 4.25% to a high of 4.50%.

We will likely see this prime rate increase when the Central Bank meets on January 25, 2023. There is some early speculation that there could be an additional 0.25% increase on March 8, 2023, however, it is too early to forecast this second 2023 rate increase.

The main tool we have when reading the current mortgage rate market is the Government of Canada Bond Yield. The Canadian bond is a government debt security that pays a return to an investor. The ‘%’ based return is called the ‘yield’ and it is considered to be one of the safest investments because the Government would have to go bankrupt, in order for it not to pay its investors.

The Government of Canada's 5-year Bond Yield factors in all known economic data on a day-to-day, and even a minute-to-minute basis. Simply put – when the market/ bond traders think that the Central Bank of Canada will increase rates, the Bond Yield increases. When the Bond market thinks the Central Bank rate will decrease, then the yield drops. In other words, the Bond yield trades, or is priced in anticipation of where the Central Bank of Canada rates will move. The Central Bank of Canada makes its rate decisions, based on the status of the economy.

Currently, as seen in the Yield chart below, the Canadian Bonds are priced in anticipation of a further 0.25% increase in Central Bank of Canada rates in early 2023 or perhaps slightly higher.

A slowing economy, lower inflation and lower Bond Yields. What does this mean for mortgage interest rates?

With lower spending comes a slowing economy and lower inflation, and eventually, lower mortgage interest rates.

Current high rates will lead to lower rates – by design.

As of January 2023, there is a growing consensus among big banks that a recession in Canada will happen in 2023. The big banks have a unique real-time view of massive amounts of cardholder spending data and are well-positioned to report on economic trends sooner. In summary, what we are hearing is that spending is decreasing significantly due to higher costs throughout the economy and higher interest rate expenses, to the point of an overall economic slowdown.

As consumer demand drops, prices of many economic inputs such as oil, copper, steel, silver, lumber, microchips, shipping costs and many other commodities have fallen drastically. These trends are very anti-inflationary. However, housing costs (ie. rents), food costs and travel/leisure activity continue to be strongly inflationary. Likely there will be a point in 2023 when these more inflationary areas of the economy cool off.

It is known in economics and recently mentioned by the Central Bank of Canada, that it takes approximately 1 year for a single interest rate hike to ‘trickle through’ or have a full effect on slowing an economy. While the first small 0.25% interest rate hike in Canada happened in March 2022, as of January 2023, we have really only seen about 9 months of effects of the more significant ‘super-sized’ rate hikes, let alone the effects of a full year of multiple rate increases. So it is important to keep in perspective that:

(1) The previous rate hikes we have seen have not had their full effect on slowing the economy, and we are already seeing a recession on the near-term horizon.

(2) The markets are expecting another 0.25% of a rate increase before stopping.

Accordingly, the narrative is also shifting away from the likelihood of a ‘soft recession’ in 2023 towards a harder-felt recession. At the point of a more severe recession, inflation is likely to be reduced significantly.

So what does this mean for mortgage rates?

What goes up to slow the economy, will eventually come down to stimulate the economy.

The Central Bank of Canada (and the Federal Reserve in the USA) is determined to fight inflation, which is why they are seen as slamming the breaks on the economy as a whole. There is no doubt this, unfortunately, will be painful for many. However, low inflation is needed on a foundational level to enjoy another long-term run of low interest rates.

Eventually, the Central Banks will begin lowering rates again to stimulate the economy and pull us out of the recession. This means lower mortgage interest rates.

More specifically, once the Central Bank reaches its peak rate or ‘terminal rate’, historically, it takes on average 6 months for the Central Bank to start lowering rates again.

In 2023, Bond markets are currently projecting the first Central Bank rate drop in November. This would mean a full 10 months at the peak rate – longer than the 6-month peak rate average.

However, to take a more careful and conservative projection, it could be January 2024 before the first Bank of Canada rate drop.

So given current market conditions, a good reference point would be between November 2023 and January 2024 for the first-rate drop.

However, if the economy slows harder and faster than expected, we could see the Central Bank lower rates sooner in 2023.

While the variable rate mortgage is directly affected by the Central Bank decisions, we will likely see 3-5-year fixed rates generally float lower throughout 2023. Because fixed rates are ‘pegged’ to the Government of Canada Bond Yields and Bond Yields trade in anticipation of Central Bank rate decisions, we will see fixed rates move lower much sooner.

Rates will not normalize at the lowest levels seen during COVID-19. However, as fixed mortgage rates approach a highly restrictive 5.5 – 6% range, the expectation is that rate normalization may occur into the low to mid ‘neutral rate’ range, or in the low 3% range for mortgage rates.

The CIBC Capital Markets projection from April 2022, seen just below, illustrates a good representation of this forecasted rate trend. However given stubborn inflation, the Central Bank rate peak will clearly be higher than in the numbers indicated in the chart:

Again, while the exact numbers are not coming in as was expected in April 2022, the main thing to note from the chart is that the rates and bond yields are increasing into 2023, but then towards the end of 2023 and into 2024, the bond yields are forecasted to drop, prompting a decrease in the Central Bank of Canada rate. This bigger-picture rate trend is the primary idea behind the chart.

How to reduce your risk against mortgage interest rate increases and save the most on your mortgage.

At this time of higher rates, unfortunately, there is no good low rate to lock into. With this said, a calculated approach may be considered to position yourself to take advantage of lower rates once they begin to fall.

According to the Central Bank, it could take until late 2023 and into 2024 for inflation to fall substantially and for their prime rates to drop.

A Fixed Mortgage Rate Strategy to Reduce Interest Rate Risk

The traditional thinking is that a 5-year rate is a safer bet. However, from the ‘rate drop’ perspective analyzed, if you lock in a higher rate for too long, there is a risk of paying too much.

Therefore a shorter term, 3-year fixed rate, for example, could position you better to renew into a lower fixed rate in 3 years’ time. For example, if your rate today is locked in at 4.59%, you would not see further upside on your rate for the next 3 years. This zero upside potential comes with the peace of mind many Canadians are looking for with their rate.

With this said, it is likely that rates will be down, perhaps 1% or even more in 3 years time, in 2026. So on your renewal date, at the end of the 3-year term, you would be better positioned to renew at a lower rate and potentially save thousands of dollars, versus remaining locked into a higher 5-year fixed term, for another 2 years.

A Variable Rate Strategy to Reduce Interest Rate Risk

For those with a higher tolerance for risk, a variable rate is worth considering because the savings could be substantial.

As we near the end of the most stunning rate increase cycles in history, the variable rate should stabilize. Then, as soon as the rate begins to fall, perhaps in late 2023 or early 2024, the variable rate holder will benefit immediately. This ‘lower rate sooner’ potential could lead to more savings than locking in even a shorter-term fixed rate.

Given over 40 years of historical rate data, as seen in a York University study on Canadian interest rates, the variable rate is likely to lead to more significant savings over the medium–long term.

There is certainly the potential for substantially more savings in the variable, but with higher variable rates currently and another 0.25% increase projected in January, it will take a thicker skin in 2023 to realize these savings over the next 1-3 years